SOLIDECN

Senior member

- Messages

- 2,879

- Likes

- 0

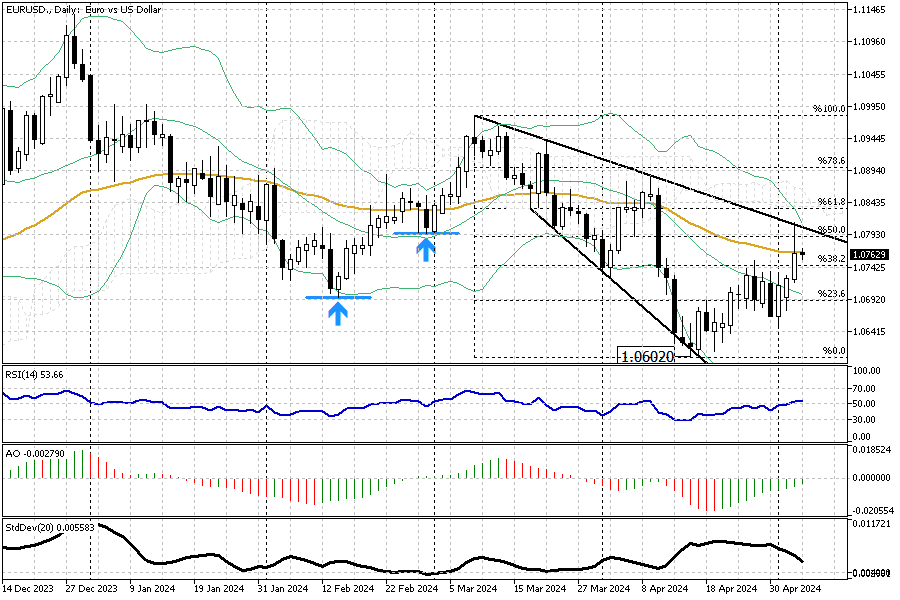

US Jobs Data Weakens Dollar

Solid ECN – The euro recently climbed towards $1.08, reaching its highest since April 9th. This rise comes as traders adjusted their forecasts for potential cuts in interest rates, influenced by a surprisingly weak US jobs report. The latest figures showed that the US economy added only 175,000 jobs last month, falling short of expectations. This underperformance has led investors to anticipate that the Federal Reserve might reduce interest rates earlier than previously thought, possibly as soon as September.

Impact of US Economic Data

The jobs report showed fewer jobs created and indicated that annual wage growth has slowed to 3.9%. Additionally, the jobless rate unexpectedly increased to 3.9%. These factors contribute to a growing belief among traders that the US economy might need stimulus sooner rather than later, influencing currency values.

European Economic Stability

Contrastingly, in Europe, economic indicators have been more stable. Recent data revealed steady inflation rates and moderate GDP growth within the Eurozone. These factors strengthen the argument for the European Central Bank (ECB) to consider reducing interest rates by June. As a result, the euro has gained strength against the dollar, reflecting differing economic forecasts between the US and Europe.